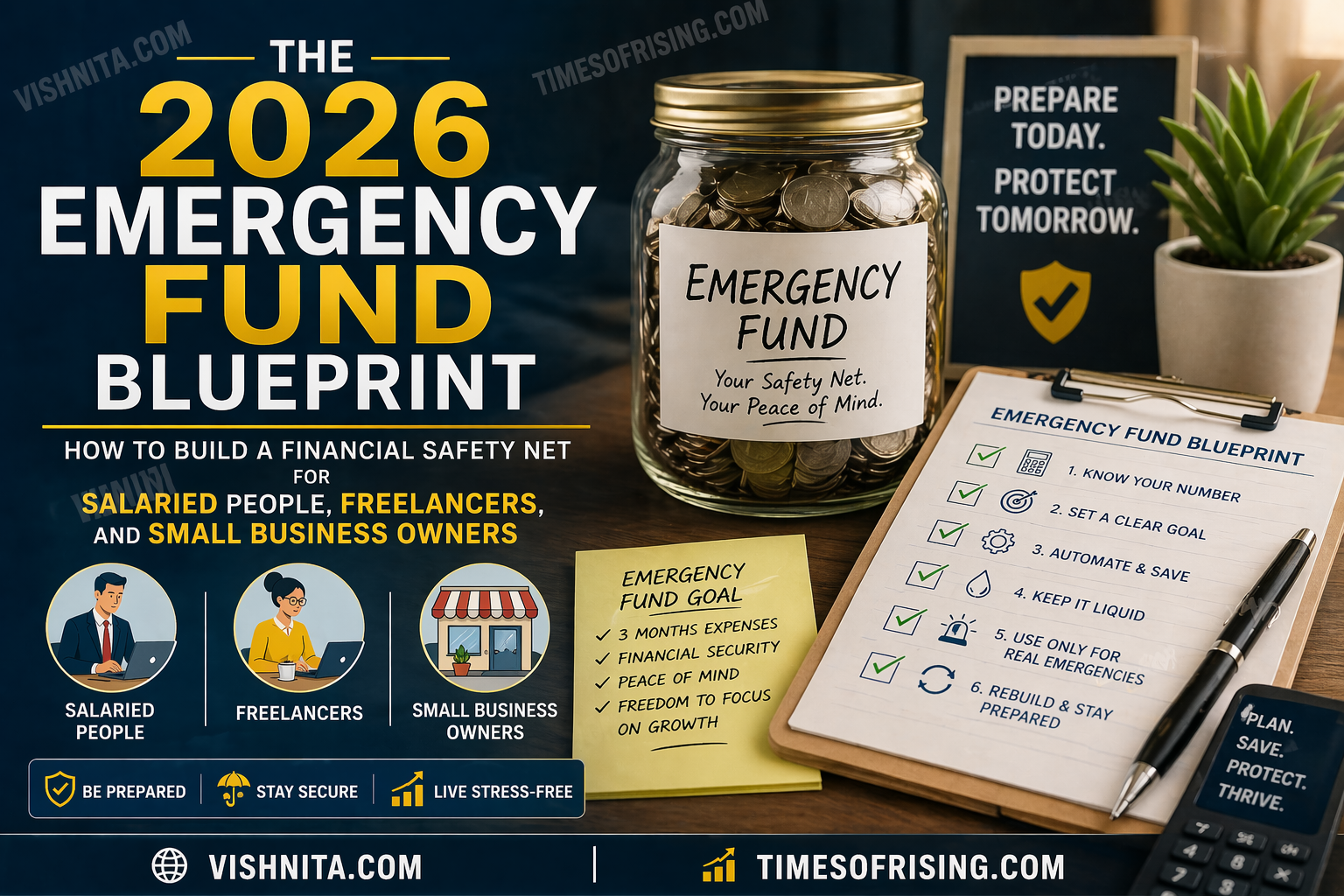

If you haven’t yet built your financial safety net, start here → The 2026 Emergency Fund Blueprint

The Real Game Is Not Income. It’s Control.

Let’s get brutally honest.

Most people don’t have a money problem. They have a cash flow problem disguised as a lifestyle problem.

You can earn ₹20,000 or ₹2,00,000 — if your money leaks faster than it flows, you’re stuck.

And in 2026, this problem is getting sharper:

- Crypto is maturing into financial infrastructure

- Businesses are focusing on liquidity and efficiency

- Stablecoins and digital payments are changing how money moves

Yet most individuals still operate like… amateurs.

This article is your upgrade.

What Is Cash Flow (And Why It’s Your Real Power)

Cash flow = money in – money out – timing gap

Not just income. Not just savings. Timing. Control. Liquidity.

Even billion-dollar companies collapse because of poor cash flow—not because of a lack of profit.

And here’s the kicker:

👉 Stablecoins and tokenised money are being used for treasury and liquidity management globally.

👉 Businesses are integrating crypto rails for faster settlement and capital efficiency

So if companies are upgrading how they manage money…why are you still winging it?

The 2026 Shift: Money Is Becoming Programmable

We’re entering a new era:

- Money moves 24/7

- Payments settle instantly

- Capital flows globally

Stablecoins alone processed $27.6 trillion in transfer volume recently

That’s not hype. That’s infrastructure.

And experts expect crypto to integrate deeper into payments, commerce, and financial systems in 2026

Translation:

Money is no longer static.

It’s dynamic, fast, and strategic.

If you don’t adapt, you fall behind.

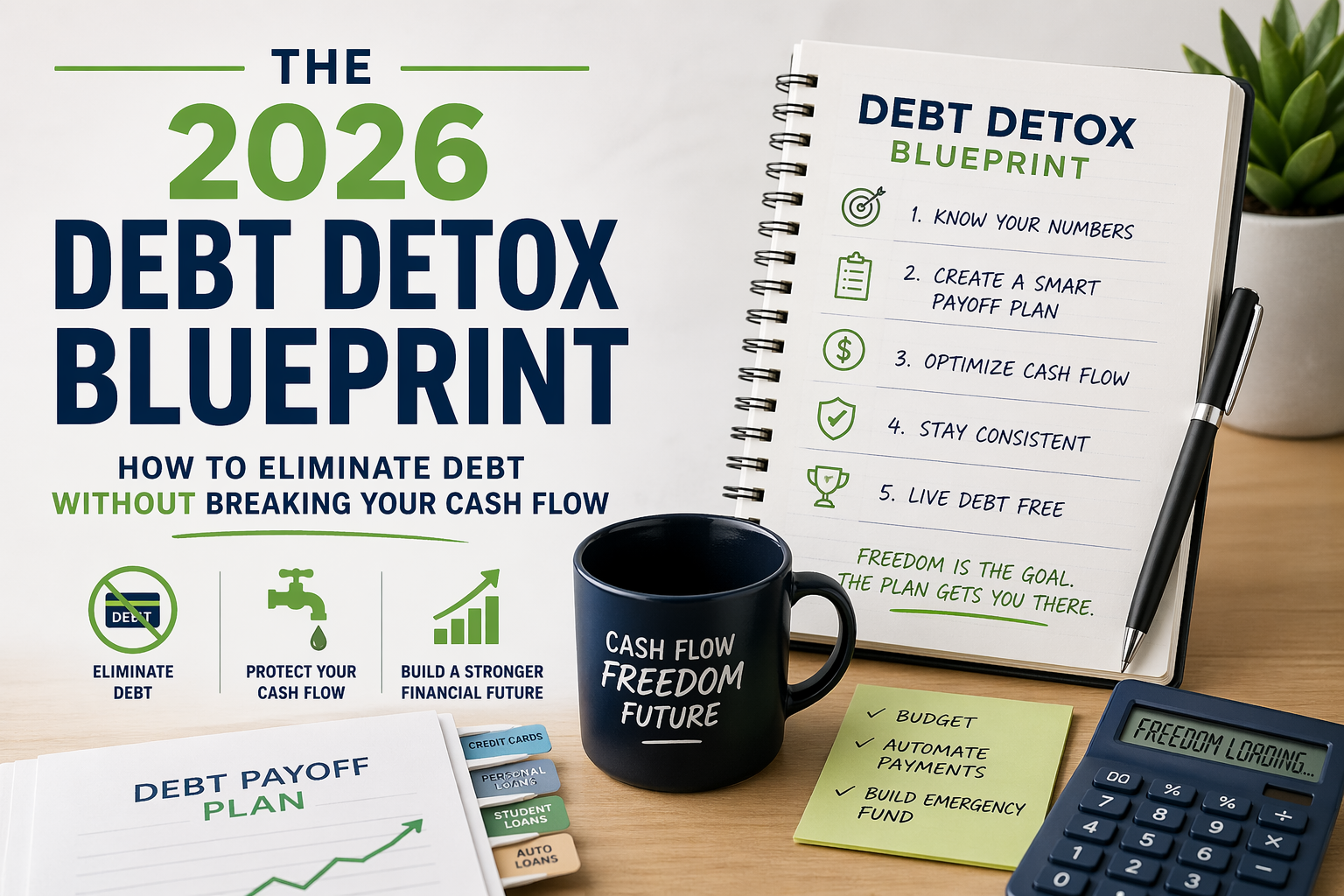

The Cash Flow System (That Actually Works)

Forget complicated budgeting apps.

Here’s the CFO-style system you need:

1. The 4-Account Framework

Divide your money into:

- Income Account – where money enters

- Survival Account – essentials (rent, food, bills)

- Growth Account – investments, business, skills

- Freedom Account – lifestyle, fun, rewards

Why this works:

It forces intentional allocation.

No confusion. No emotional spending.

2. The 60-20-10-10 Rule (Customizable)

- 60% → Survival

- 20% → Growth

- 10% → Emergency/buffer

- 10% → Lifestyle

And yes — this connects directly to your previous article:

👉 Without a buffer, your system collapses👉 That’s why your emergency fund is step zero

(Read again → https://timesofrising.com/2026-emergency-fund-blueprint/)

3. Cash Flow Timing Strategy (The Hidden Weapon)

This is where amateurs lose.

Example:

- Salary comes on the 1st

- Expenses hit on the 5th

- Investments delayed → never happen

Fix:

- Auto-transfer to savings within 24 hours

- Delay expenses if possible

- Front-load investments

Control timing = control life.

For Freelancers & Creators: Build a “Volatility Buffer”

Your income is unpredictable.

So your system must be stronger.

Strategy:

- Save 30–50% of high-income months

- Create a 3-tier buffer

- Monthly survival buffer

- Business buffer

- Personal emergency fund

Why?

Because income volatility is the real risk, not low income.

For Small Business Owners: Think Like a Treasury Manager

Stop thinking like a shopkeeper.

Start thinking like a financial operator.

Your business must track:

- Cash inflow cycles

- Payment delays

- Inventory lock-in

- Fixed vs variable costs

And here’s where 2026 gets interesting:

👉 Stablecoins are now being explored for B2B payments and treasury operations

👉 Companies may soon need to disclose stablecoin holdings as cash equivalents

That means:

Crypto is entering real business finance.

Not speculation. Infrastructure.

Should You Use Crypto for Cash Flow?

Short answer: Partially. Carefully. Strategically.

Use crypto for:

- Cross-border payments

- Fast transfers

- Diversification

Don’t use crypto for:

- Emergency funds

- Essential expenses

- Short-term survival

Because:

👉 Stablecoins can still face risks like reserve issues, regulation, and de-pegging

👉 Even experts warn about volatility and uncertainty in crypto markets

The Smart Hybrid Strategy (This Is the Edge)

Combine:

- Traditional finance (bank, savings) → stability

- Crypto rails → speed & optionality

- Cash reserves → survival

This is how modern money works.

Not either/or.

But stacked systems.

The Biggest Cash Flow Mistakes (Stop Doing These)

Let’s call it out.

1. Treating income as wealth

Income ≠ control

2. Investing without liquidity

You’re one emergency away from selling assets at a loss

3. Mixing personal and business money

This kills clarity

4. Ignoring timing

Cash flow is about when, not just how much

5. Over-relying on crypto hype

Crypto is a tool—not a foundation

The 30-Day Cash Flow Reset Plan

If you want results fast, do this:

Week 1:

- Track every rupee

- Identify leaks

Week 2:

- Set up 4 accounts

- Automate transfers

Week 3:

- Build a starter emergency fund

- Cut 2 unnecessary expenses

Week 4:

- Allocate for growth

- Create a buffer strategy

Repeat monthly.

That’s it.

No fancy tricks.

Just discipline + systems.

How This Article Helps You Rank (And Monetise)

Let’s talk strategy.

This article is designed to:

1. Capture multiple keywords:

- cash flow management

- personal finance system

- money management 2026

- small business cash flow

- crypto payments

2. Build topical authority:

It connects:

- emergency funds

- crypto

- business finance

3. Increase engagement:

- actionable frameworks

- relatable examples

- structured system

4. Drive monetisation:

- perfect for fintech sponsorships

- crypto tools

- budgeting apps

- financial services

The Real Truth (No Sugar-Coating)

You don’t need more money.

You need:

- Better systems

- Better discipline

- Better decisions

Because money doesn’t change people.

It reveals them.

Final Thought

Cash flow is not math.

It’s behaviour.

It’s awareness.

It’s control.

And once you master it…

You stop chasing money.

And start directing it.

[…] Also Read: The 2026 Cash Flow System: How to Control Money Like a CFO (Even If You Earn ₹10,000 or ₹10 Lakh… […]