When money feels unstable, people do one of two things: panic or plan. The smart move is planning.

An emergency fund is not boring. It is power. It is the quiet buffer that stops one medical bill, one lost client, or one broken machine from becoming a financial disaster. In a year where many households still feel uneasy about savings and small businesses are balancing growth with pressure on cash flow, a real emergency fund is not optional. It is the foundation.

What an emergency fund actually is

An emergency fund is money kept aside for genuine surprises: job loss, a sudden repair, a family emergency, or a temporary drop in income. It is not for shopping, not for “just one small trade,” and not for emotional decisions disguised as financial strategy.

For most people, the money should live in a liquid, federally insured account. The FDIC says deposit insurance protects deposits at insured banks up to at least $250,000 per depositor, per bank, and financial experts generally recommend keeping at least six months of living expenses in a federally insured product such as a savings account or CD.

Why this matters more in 2026

The financial mood in 2026 is simple: uncertainty has not been cancelled

Bankrate’s 2026 Emergency Savings Report found that 60% of Americans are uncomfortable with the level of their emergency savings, which tells you the problem is not rare; it is mainstream. At the same time, small-business outlook pieces in 2026 keep pointing to cash flow, working capital, and operational efficiency as major priorities.

That is why this topic has both evergreen search value and current relevance. People are not just searching for “how to save money.” They are searching for “how do I survive uncertainty without falling apart.”

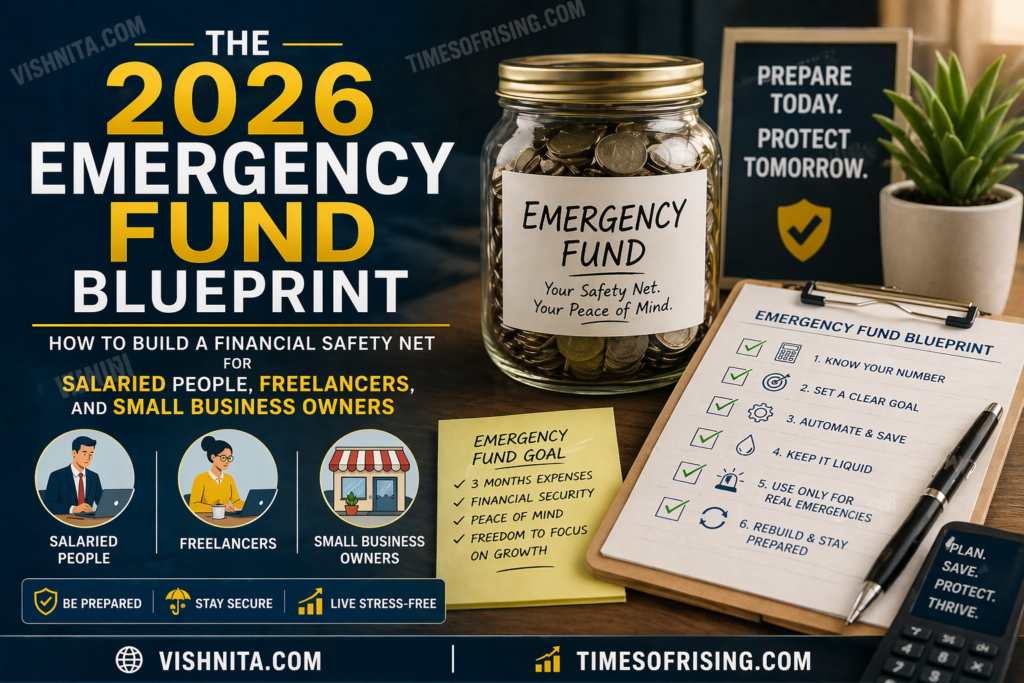

How much emergency fund do you really need

Forget the fake guru math. The right amount depends on your income stability.

If you have a steady salary, start with one month of expenses, then move to three months, then six. If you are a freelancer, creator, salesperson, or small business owner with irregular cash flow, aim higher. Income volatility means your emergency fund should be more aggressive, not less.

A simple rule:

- Salaried employee: 3 to 6 months of essential expenses

- Freelancer/gig worker: 6 to 9 months

- Small business owner: 3 to 6 months of business operating costs, plus a personal buffer

This is not about fear. It is about the runway.

Where to keep emergency money

Keep it boring. Boring is the point.

The safest place is usually a separate savings account or another federally insured cash product. The FDIC-backed approach is designed for access and protection, not excitement. Treasury I Bonds can also be part of a longer-term safety strategy because their interest rate changes every six months based on inflation, and they can be cashed after 12 months, though redeeming before five years means losing three months of interest.

Money market funds can be useful for some investors, but the SEC notes they are mutual funds and the risk profile is different from a bank deposit. That is why the best emergency fund is usually the one you can access quickly without turning it into a side quest.

Should you keep emergency money in crypto?

No. Not the core fund.

Stablecoins are getting more attention in payments and treasury discussions, but current reporting still shows most stablecoin activity is tied to trading and infrastructure, not mainstream household emergency planning. Reuters reported that even as banks and regulators engage more with stablecoins, their real-world payment use remains limited. The BIS has also warned that stablecoins can create fragmentation and financial stability risks if coordination is weak.

Translation: Crypto may belong in a portfolio. It does not belong as the thing that keeps your rent paid when life gets messy.

How to build the fund faster

Here is the clean system.

First, automate it. Money should move before you can overthink it.

Second, separate it. A separate account creates friction against impulse spending.

Third, name it correctly. “Emergency Fund” is strong. “Vacation someday maybe” is weak.

Fourth, build it in layers:

- Starter layer: ₹10,000 / $500 / one small bill cycle

- Stability layer: one month of expenses

- Resilience layer: three to six months

- Business layer: extra reserve for owners and freelancers

The fastest way to build it is not by motivation. It is by systems: automatic transfers, windfalls, cuts to recurring waste, and every income spike split before lifestyle inflation can eat it alive.

For small business owners: treat cash flow like oxygen

A business without a reserve is one delayed payment away from stress.

If you own a small business, your emergency fund should not be mixed with everyday spending. Build a separate reserve for payroll gaps, inventory shocks, repair costs, and slow months. 2026 small-business reporting keeps pointing toward cash flow discipline, access to capital, and AI-enabled efficiency as survival levers.

The best small businesses do not just chase revenue. They protect margin, timing, and liquidity. That is what keeps the doors open when the market gets weird.

The real mindset shift

An emergency fund is not money sitting idle.

It is money standing guard.

It gives you time to think. It stops panic-selling. It keeps you from borrowing at the worst possible moment. It protects your family, your business, and your future self from today’s bad surprise becoming tomorrow’s debt spiral.

That is why this topic never dies. It is evergreen because human life is unpredictable. It is trending because uncertainty is still very much in the room.

FAQ

How much emergency fund should I have?

Most people should aim for 3 to 6 months of essential expenses. Freelancers and business owners usually need more.

Where should I keep it?

In a separate, liquid, federally insured account. Keep the goal of safety and access, not maximum return.

Can I use crypto for emergencies?

Not for the core fund. Crypto is too volatile for money you may need at short notice. Stablecoins are still mainly tied to trading and infrastructure, not standard household emergency planning.

What is the first step if I have nothing saved?

Start with one tiny target: a starter buffer. A small reserve is better than no reserve.