Debt does not always look dangerous at first.

It often looks normal.

A credit card here. A personal loan there. A business line of credit “just for now.” A buy-now-pay-later plan that feels harmless because the payment is small. Then one day, the monthly due dates start running your life instead of the other way around.

That is the trap.

In the United States, total household debt reached $18.8 trillion in the fourth quarter of 2025, according to the New York Fed, and credit card balances alone stood at $1.28 trillion. Consumer credit also continued to grow in February 2026, indicating that borrowing pressure remains very much alive.

That is why this topic matters now. Not just for search traffic, but for real people trying to stop money leaks before they become life problems. And yes, it connects directly to your earlier articles on the Emergency Fund Blueprint and the Cash Flow System. If those are the foundation, this is the cleanup crew.

Start here after reading the earlier pieces: “/2026-emergency-fund-blueprint/” and “/the-2026-cash-flow-system-how-to-control-money/”.

Debt is not just a number. It is a system failure.

Most people think debt is the problem.

Usually, debt is the symptom.

The deeper issue is a broken money system: you spend before you plan, borrow before you stabilise, and invest before you protect.

That is why a debt payoff plan cannot be just “pay everything fast.” That sounds good on a motivational poster. Real life needs structure.

The Federal Reserve’s Beige Book reported that credit standards had tightened somewhat across loan types and that delinquency rates remained elevated in some categories. In other words, borrowing conditions are not getting magically easier for everyone.

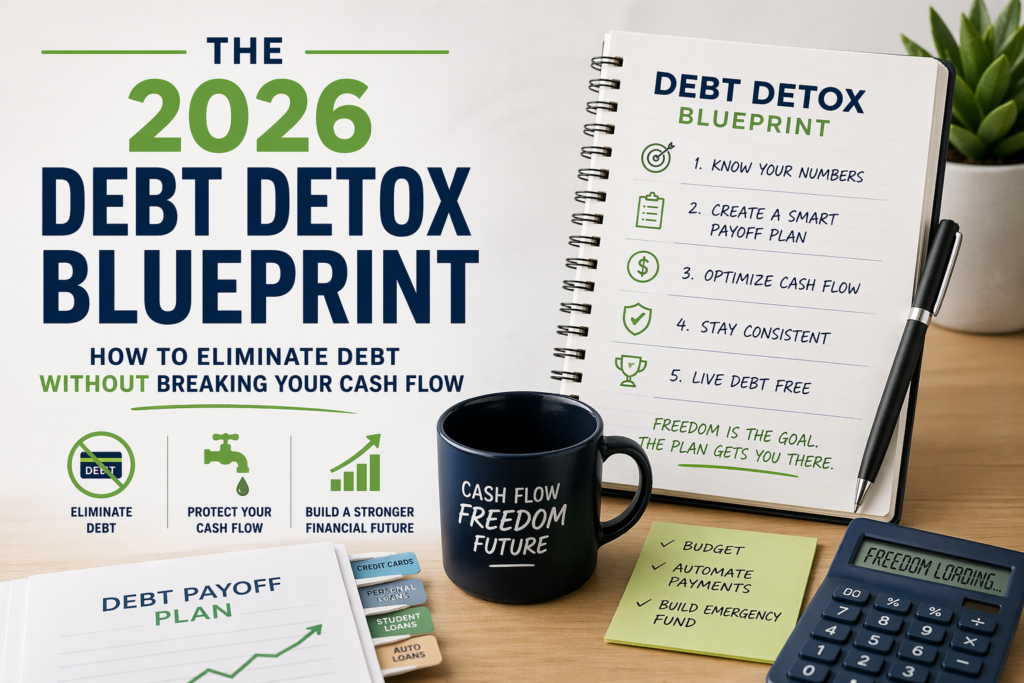

So the smartest move in 2026 is not emotional hustle. It is a clean debt detox.

What a debt detox actually means

A debt detox is not some dramatic no-spend monk fantasy.

It means:

- stopping new debt from getting created

- attacking expensive debt first

- keeping cash flow alive while you repay

- protecting your emergency fund

- avoiding replacement debt that only moves the pain around

That last part matters.

Paying off a card by draining every rupee and then re-borrowing for the next emergency is not progress. It is debt cosplay.

Step 1: Freeze the leak

Before you repay anything, stop the bleeding.

That means:

- No new credit card swipes for non-essential items

- No fresh personal loans for lifestyle purchases

- no borrowing to “invest” in crypto, stocks, or side projects

- No mixing business expenses with personal spending

This is especially important now because consumer credit is still expanding, and revolving debt is still moving. The New York Fed’s data shows credit card balances increased by $44 billion in Q4 2025 to $1.28 trillion, which is not the sign of a world that has suddenly become financially calmer.

Step 2: Know the debt types you are actually fighting

Not all debt deserves the same treatment.

High-interest debt is the fire. Low-interest debt is the smoke. Business debt can be either a tool or a trap.

A simple order of attack usually looks like this:

- Credit cards

- Personal loans with high APRs

- Buy-now-pay-later balances

- Auto loans

- Education loans

- Low-rate secured debt

If a debt is charging a brutal rate, it is not “manageable.” It is expensive.

Step 3: Choose the right payoff strategy

There are two classic methods.

Snowball

Pay off the smallest balance first.

Best for:

- motivation

- visible wins

- people who need momentum

Avalanche

Pay off the highest-interest debt first.

Best for:

- saving more money over time

- disciplined users

- mathematically optimal payoff

Here is the real-world move: use a hybrid.

If you are overwhelmed, start with one fast win to build belief. Then switch to the highest-interest debt. Psychology gets you started. Math gets you finished.

Step 4: Keep cash flow alive while you pay debt

This is where your previous article matters.

If your cash flow is messy, debt payoff will collapse under pressure. Your Cash Flow System article should sit right before this one in the reader’s path because debt is easier to kill when your money is already organised.

A clean structure is:

- essentials first

- minimum debt payments second

- emergency savings third

- aggressive debt payoff fourth

That sounds slower than the “kill everything at once” crowd, but it is far more sustainable.

Step 5: Do not use crypto as a debt escape hatch

This is where people get reckless.

Crypto can be part of a broader investment strategy, but it should not become a debt roulette table. Stablecoins are getting more attention in payments and treasury discussions, and Stripe notes that stablecoin transfer volume reached $27.6 trillion in 2024. But that same ecosystem is still under serious regulatory and financial-stability scrutiny. Reuters reported that the BIS recently warned about fragmentation, risk, and the need for global coordination around stablecoins.

Translation: crypto is changing. That does not mean debt should be solved by gambling on volatility.

Use crypto in the investment bucket. Do not use it as emergency debt medicine.

Step 6: Small business owners need a separate rulebook

If you run a business, personal debt and business debt can destroy each other if you mix them.

A small business debt detox should separate:

- personal spending

- business operating costs

- tax reserves

- debt service

- working capital

J.P. Morgan’s 2026 business outlook highlights the importance of unlocking cash and managing liquidity, and its cash flow guidance stresses forecasting and resilience. Paychex also points to 2026 small-business trends centred on AI integration, compliance, and operational efficiency.

So for business owners, debt payoff should never starve operations. If the business collapses, the debt payoff plan becomes a funeral speech.

A 30-day debt reset plan

Days 1 to 3: Audit everything

List every debt, balance, minimum payment, and interest rate.

Days 4 to 7: Stop new leakage

Freeze unnecessary spending and remove frictionless borrowing.

Days 8 to 14: Protect cash flow

Build or preserve a small emergency buffer so one surprise does not send you back to debt.

Days 15 to 21: Attack the target debt

Choose snowball or avalanche and make the first real extra payment.

Days 22 to 30: Automate the system

Set payment dates, auto-transfers, and account separation so the plan continues without willpower.

The emotional truth nobody likes saying out loud

Debt is exhausting because it steals future income.

Every payment is a little piece of tomorrow already spent.

That is why debt freedom is not just a financial achievement. It is a psychological reset. Once debt pressure drops, your brain gets quieter. You think better. You sleep better. You stop making fear-based decisions.

That is the real prize.

Also Read: The 2026 Cash Flow System: How to Control Money Like a CFO (Even If You Earn ₹10,000 or ₹10 Lakh)